Most property owners believe tax planning is only relevant when they choose to sell. But one of the most overlooked and misunderstood sections of the Internal Revenue Code applies when the decision is made for you.

I’m talking about the 1033 Exchange, a powerful but under-utilized provision that comes into play when a property is taken through eminent domain or destroyed through an involuntary event. If you own investment or business real estate, understanding this rule before you’re forced into a sale can mean the difference between preserving capital and writing a check to the IRS you never planned on.

Let’s break it down, plain English, real-world application, no fluff.

What Is a 1033 Exchange?

A 1033 Exchange applies when property is involuntarily converted. In real estate, that most commonly happens through eminent domain, where a government entity acquires private property for public use, think highway expansions, infrastructure projects, rail lines, utilities, or redevelopment initiatives.

Unlike a traditional sale, the property owner doesn’t initiate the transaction. The government does. And because the owner didn’t choose to sell, the tax code provides a form of relief.

Under Section 1033, if your property is taken and you reinvest the proceeds into a qualified replacement property, you may be able to defer capital gains taxes, similar in spirit, but not identical, to a 1031 Exchange.

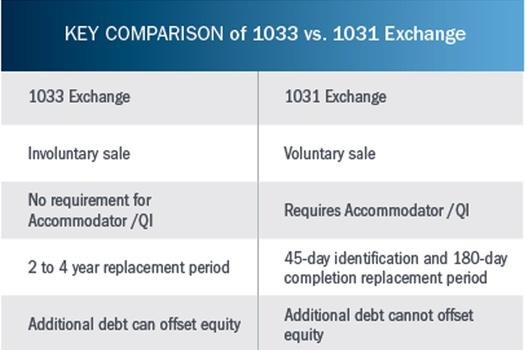

How a 1033 Exchange Is Different from a 1031

This is where things often get confused.

A 1031 Exchange is elective. You decide to sell. You follow strict timelines: 45 days to identify, 180 days to close. You must use a qualified intermediary. The rules are rigid, and mistakes are costly.

A 1033 Exchange, by contrast, is reactive. The triggering event is involuntary. And because of that, the IRS allows far more flexibility.

Here are a few key differences:

• Longer replacement period: Instead of 180 days, a 1033 typically allows up to two years, and in some cases three years, to acquire replacement property

• No qualified intermediary required: Proceeds can be held by the taxpayer

• More flexibility in timing: Replacement can occur before or after the property is taken

• Still requires reinvestment: To fully defer tax, proceeds must be reinvested into property that is similar or related in service or use

That flexibility is a gift, but only if you understand how to use it properly.

What Qualifies as Replacement Property?

This is another area where planning matters.

Generally, replacement property must be similar or related in service or use. In practical terms, that usually means reinvesting into business or investment real estate. The IRS interpretation here can vary depending on whether the owner is an investor or an owner-user, which is why professional guidance is critical.

If the replacement property costs less than the amount received from the eminent domain taking, the difference may be taxable. To fully defer capital gains, you must replace equal or greater value.

Sound familiar? It should. The principle mirrors a 1031, even though the mechanics differ.

Why Most Property Owners Miss This Opportunity

Here’s the hard truth: most property owners don’t plan for eminent domain until it’s already happening.

They receive a notice.

They negotiate a payout.

They close.

And only after the funds are in hand do they ask, “What about the taxes?”

By then, options may be limited or lost entirely.

The most successful 1033 outcomes happen when owners engage advisors early, before accepting proceeds, before signing agreements, and before assuming the check equals profit.

The Bigger Picture: Forced Sales Still Deserve Smart Planning

Whether it’s a voluntary sale under a 1031 or an involuntary conversion under a 1033, the objective is the same: preserve capital, control timing, and protect long-term wealth.

A 1033 Exchange is not a loophole.

It’s not aggressive.

And it’s certainly not new.

It’s a recognition by the tax code that when the government takes your property, you shouldn’t be penalized for rebuilding elsewhere, if you do it correctly.

Final Thought

Eminent domain is disruptive. It’s emotional. And it often arrives without warning. But tax consequences don’t have to be part of the damage.

If you own investment or business property and there’s even a hint that eminent domain could be in your future, the time to understand the 1033 Exchange is now, not after the fact.

At Best1031Online.com, education comes first, because smart planning doesn’t begin at closing. It begins the moment a property owner understands their options.

And in the case of the 1033 Exchange, those options can be far more powerful than most people realize.

–

We Are Here to Help!

If you are an investment property owner, schedule a no-obligation strategy call with me at www.Best1031Online.com, or contact James Bean of SVN-Rich Investment Real Estate Partners, CA DRE# 01970580, at 805-779-1031 or email at james.bean@svn.com.

If you are an agent/broker, I am happy to discuss strategies with you on how to best serve your next listing client in preparing them for a successful exchange. Please visit the site and click on the Agent’s button located at the top right-hand corner of the Home Page.

Don’t know what certain terms mean?

Click here for a Glossary of Terms:

https://svn-best1031online.com/glossary/

Stay Connected with Best 1031 Online!

Want more insights on 1031 Exchanges, real estate strategies, and smart planning to preserve both wealth and family harmony?

Subscribe to my YouTube channel, Best 1031 Online!, where I release monthly episodes of QI Corner and other expert content designed to keep you informed and ahead of the curve.

I cannot do this alone!

This Channel would not exist if it weren’t with the daily support of CRE Task Wizard!

Go visit CRE Task Wizard at https://cretaskwizard.com/ to see how they can get you doing what you are best at, doing deals!

Please stay tuned and follow me on LinkedIn, X, Instagram, TikTok & Facebook @1031BrokerJames.

All information is deemed to be accurate and is not tax or legal advice. All investors/taxpayers should consult their CPA, tax attorney, and investment advisors.